Medicare is a federal health insurance program that pays for a variety of health services that are covered.

Various Types of Medicare Plans

First things first, what is Medicare?

Medicare is a program of public health insurance that pays for many health programs provided. Generally, if you or your spouse) have served for at least 10 years and paid taxes to support your Medicare coverage, you are 65 years old or older, and a U.S. citizen or permanent resident, you are eligible for Medicare.

It is not just necessary to choose the right plan, it's personal. It is best to know all your choices in order to figure things out. So what are the variations between Medicare Parts A, B, C, and D?

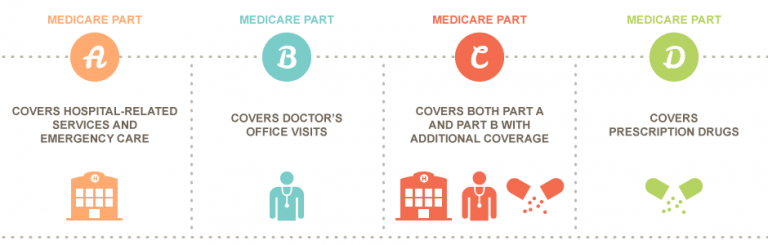

ORIGINAL MEDICARE — your government plan—is only PART A and PART B.

Medicare Part A is hospital coverage.

Medicare Part B is medical coverage. You must pay a premium each month.

Medicare PART C combines your hospital, medical, and typically even your drug coverage into one complete plan. You may need to pay an additional premium each month.

Medicare Part D is prescription drug coverage only.

Consider Medicare Advantage (PART C) as coverage for ALL-IN-ONE.

You get coverage for hospital and basic medical treatment, such as preventive services and inpatient and outpatient care, plus several plans provide extra vision, dental, and hearing benefits. You get all the advantages of Original Medicare, plus consistent copayments that make budgeting easy, a limit on your maximum out-of-pocket, and preventive screening coverage.

Medicare Supplement or Medigap programs still exist. These forms of policies have an extra premium, but only cover the expenses of any of the care not covered by Original Medicare. No extra benefits or optional benefits are always included with these programs. There is no one-size-fits-all solution when it comes to Medicare. To better understand your choices and decide what's best for YOU, give us a call or work with a licensed insurance agent.

What’s Your Medication Situation?

On a daily basis, many of us take one or more drugs. To ensure that no coverage modifications have occurred, it is necessary to review the annual drug form. Be sure to verify the following while checking your prescription form:

-

Prior authorization requirements (additional hoops to jump through)

-

Limited pharmacy access (some drugs are only available at specific pharmacies)

-

Prescription tiers and the associated cost

-

Drug brand names and generics

-

Drug brand names and generics

There is a range of instruments out there that allow you to compare drug costs between Medicare Advantage and Prescription Drug Plans for shopping plans.

Selecting the Right Plan for you

Things alter, people change, plans change, and life changes. What may have been a brilliant idea may no longer serve your requirements. Every year, remember to check your strategy and coverage. Just like when you're shopping for every other program, keep your eyes out for:

-

Monthly premiums: This is the monthly insurance policy bill that you pay for (to be a member of an insurance plan).

-

Maximums of Out-of-pocket (OOP): This is the average amount you will pay per year for the benefits provided by your contract. To the out-of-pocket limit, sums you pay for your premiums, coinsurance, and copays refer. There are separate medical and pharmacy deductibles in some plans, and some programs may not be available to or may surpass the limit OOP.

-

IN-NETWORK VERSUS OUT-OF-NETWORK: On the network of your contract, in-network or participating networks and facilities participate. These providers must write off in other words, they can not charge you for) payments that surpass the permitted sum (these are called excess fees) for covered services. If a provider is out-of-network, he or she does not participate in the network of your contract and does not recognize the allowable amount as full payment. Your coverage does not cover an out-of-network provider's services, which means you may be responsible for paying the extra costs for the services.

-

Referral requirements: What if you need to see a specialist? For several plans, before you can pursue any specialized treatment, a referral from your primary care provider is required; without that prior approval, you might be responsible for footing the bill. That's an expense you'll want to stop.

-

Copay and coinsurance visit: This is the fee that you have to pay the doctor for treatment. Many plans have lower copays for providers of primary care and higher copays for providers of secondary care.

-

Annual deductibles: This is a sum that you must pay until the plan starts to pay the required payments to physicians and facilities. (But note, you still only pay the approved amount from in-network providers for covered services!) Some benefits groups might have different deductibles.

-

What about coinsurance? Although a copay is always a fixed amount, once you hit the deductible, coinsurance is typically a percentage of the cost you pay.

-

BONUS PERKS: What are the choices, instruments, and facilities that your package includes? Discover gym memberships, fitness discounts, dental and vision, and other extras. Some of these advantages might cost more. Consider items like glasses, teeth cleanings, eye checks, and other dental facilities. The necessities for vision and dental will be provided by several policies, but if you need special bifocals or a dental operation, you may end up paying through the teeth. Gym memberships or deals can be other perks. Take a look to see how your budget, lifestyle, and needs match together.

Remember: The premium you pay for your plan may not refer to the maximum out-of-pocket or other sums you would pay for covered services (see Monthly premiums). When calculating annual healthcare expenses, out-of-pocket maximums are sometimes ignored. You could end up with a "sky's the limit" out-of-pocket bill, depending on the plan you choose!

Usually, Original Medicare pays 80 percent and you pay 20 percent. But NO out-of-pocket limit exists. With Medicare Advantage, your out-of-pocket expenses are limited per year to a fixed number. When it comes time for renewal, don't forget to review your contract for those out-of-pocket costs every year.

Also Read : What to look for in a Medicare Expert?

Be in A Good Company

It is daunting to pick the best plan-it can be downright exhausting to wade through the hundreds of insurance providers. There are several categories to remember for starters:

Where everyone knows your name

Well maybe not everyone knows your name, but the benefit of going local goes back to that. Be sure to search the network of plans when comparing businesses. Are your existing network providers and services in place? If not, to satisfy your healthcare needs, are there better local providers?

Local Vs. National

Local insurance providers are familiar with and willing to use the same facilities, physicians, and resources and are partnering with them to deliver the best quality services at the most competitive rates. In order to ensure you get the service you need, local businesses also recruit local members who have the local know-how. Throughout the city, they may also provide local incentives, workshops, and services. Global corporations may not have the local experience, but with a national presence, they could have a wider reach.

For-Profit Vs. Non-Profit

Who, you or shareholders, is the priority? For-profit corporations tend to return profits to investors, while non-profits have to reinvest their profits back into the membership benefits package.

Customer Service

A big deal is customer service! Can you chat on the phone with a local person? Do you have to wait and jump through a thousand hoops only for a generic answer to be said? You need a real person to make something happen to you when you need answers.

Medicare Dates to Remember

You do not want to skip enrollment; otherwise, you're going to end up waiting for coverage for another year. So, carpe diem, as they say! In order to revisit your strategy and make changes if necessary, there is no time better than the present. It's a safe idea to contact the insurance company representative or chat with a licensed insurance agent after you've compared policies and rates. Make sure that with enough time you do all of this because you won't want to miss out on your enrollment date.

Medicare Advantage Open Enrollment Period

An enrollment period exclusively for participants of the Medicare Advantage. You have a one-off chance to change plans from January 1 to March 31. That means that you may choose to move to another Medicare Advantage plan, or you may cancel your original Medicare return plan. For prescription drug coverage, you can also add Part D during this time (if it is not included in your Advantage plan). Note that this is a one-time change of schedule every year.

First Time Medicare Registration

Turning sixty-five? You have a window of seven months during the month of your birthday.

That is three months before your month of birth, three months after your month of birth, and your month of birth, of course.

Also Read : Things To Avoid During Medicare Open Enrollment

Annual Enrollment Period

Have your calendars marked? You are authorized to make changes and to change plans every year from October 15 to December 7. This is a perfect chance to check your coverage to ensure that it still works for you.

Special Enrollment Periods

The keyword here is special. For special circumstances, these intervals are reserved. Here is a sample list of such special times of enrollment:

-

Have both Medicare and Medicaid

-

Moved out of your geographical service area

-

Lost other creditable employer or retiree insurance coverage benefits

-

Qualify for low-income prescription drug assistance

You will also have a special enrollment period when you turn 65 if you have Medicare because of a disability but are not yet 65 years old.

What You Need to Talk About SSA, HSAs, and Medicare Delay

If by the time you turn 65, you are still planning to work and are not retired, there are still a few things you need to remember.

Medicare Delaying And Late Enrollment Penalty

By continuing on the insurance plan of your employer, you will continue to work and defer Medicare. Not all employer programs, however, are the same and, in certain situations, if your coverage is not deemed creditable, you can incur a Late Enrollment Penalty (LEP). The thing about LEP is that before death, it follows you. That means that you will have to pay this penalty indefinitely if you incur an LEP. It's a good idea to send us a call or work with a licensed insurance provider to check your coverage status and prevent any lifetime fines, particularly if you intend on working beyond 65.

Social Security Administration

Your Medicare card will automatically arrive in the mail about 90 days before your 65th birthday if you collect Social Security payments before the age of 65. If you postpone Social Security until 65, what happens? Everyone's situation is special.

What happens to your HSA while you're in the Medicare?

You will no longer contribute to a health savings plan if you are on Medicare (HSA). Everything you saved in your HSA, however, can be used for the rest of your life to qualify for medical expenses. This includes paying, tax-, and penalty-free, for Medicare and Medicare Advantage premiums! But remember that in order to pay for Medicare Replacement insurance premiums, you should not use your HSA.

What’s Next?

You have your homework done, and you are set! To make sure you understand everything about your soon-to-be plan, network, incentives, and contacts,

we would like to talk with you. To get started, click the button below.

Find The Best Medicare Insurance That Suits Your Needs!