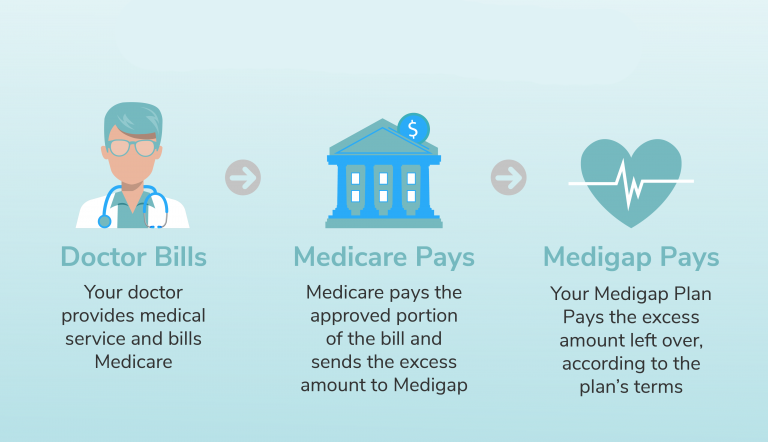

You may have learned the Original Medicare has some "gaps" in coverage. It is for this purpose that Medicare Supplement programs exist. These health insurance packages, also known as Medigap plans, are provided through private insurance providers that help cover deductibles, coinsurance, and copayments, among other items.

We've put together pointers to assist you in selecting the best Medicare Supplement package for your needs. But first, we'll go over the Medigap concept and why you should care about buying supplementary insurance.

What is Medicare Supplement Insurance Also Known as Medigap?

Medigap is a form of private health insurance that fills the gap between what Original Medicare provides and what people want in terms of health coverage. There are ten different plans to choose from, each of which is standardized.

Consider Medigap as a way to help handle your medical expenses. Rather than waiting for bills to come in following an accident or sickness, you pay a fee to the health insurance provider in order for the insurer to cover a greater portion of the overall healthcare costs.

While no Medigap program would cover all out-of-pocket costs, each one provides a different degree of insurance. You should choose the package that best fits your financial condition and health based on your budget.

Take into account the following forms of out-of-pocket expenses:

-

Copayment: You might be required to pay a copayment before receiving treatment from a provider, such as a doctor or a hospital.

-

Deductibles: A premium is an amount you must pay out of pocket before your insurance policy kicks in.

-

Coinsurance: This determines whether you are responsible for a certain amount of a medical claim. Individual Medigap policies include a variety of deductibles, copayments, and coinsurance amounts and percentages.

Medigap is not the same as Medicare Advantage. Original Medicare Part A and Part B are replaced by a Medicare Advantage plan, also known as Medicare Part C. These policies may have lower monthly rates, but they may restrict your choices even more. Many Medicare Advantage plans, for example, limit your provider options and include referrals if you need to see a specialist.

Let's look at the tips for choosing the right Medicare supplement plan now that we've covered the Medigap concept.

Find Out Which Medigap Plans Are Available In Your Area

The Medigap policies are all the same. This ensures that no matter which provider you select, all Medicare Supplement policies have the same coverage.

Private insurance providers, on the other hand, can choose which policies to sell and in which areas. Plans A, B, and F can be covered by an insurer, but only in three states.

This is why doing detailed comparison shopping is a smart idea. To narrow down your choices and get a better idea of which plans are available to you, start your search with your zip code or area.

Premiums are set by private insurance providers as well. Despite the fact that Plan A provides the same coverage if you select Insurer A or Insurer B, one insurer will charge more per month than the other.

Knowing which plans are available in your area is the best way to compare. After you've compiled a list of your options, you can compare individual policies based on premium.

Settle On The Amount Of Coverage You Need

You can decide what your health and budget require once you're familiar with the coverage levels offered by Plans A, B, C, D, F, G, K, L, M, and N. Bear in mind that you will be subject to underwriting if you intend to change your Medicare Supplement plan in the future.

It's preferable to choose a package that will serve you well after you turn 65. Let's say you've never intended to fly abroad before. In that case, having emergency medical coverage for foreign travel would be useless.

Similarly, if your regular physicians support Medicare and charge exactly what Medicare costs, you won't need an excess charges package. The disparity between what a company costs and what Medicare pays is covered by this coverage.

You should also think about your general health, any pre-existing or chronic illnesses, and your salary. A detailed part like G or F could be the best choice for you if you need to manage your money more effectively.

Become Acquainted With All Plans

Different aspects of your healthcare are covered by each Medicare Supplement package. Every other group is different, but they all cover 100 percent of your Medicare Part A coinsurance and hospital costs.

Plan K and L, for example, only cover 50% and 75% of your Medicare Part B coinsurance or copayment, respectively, while the other policies cover 100%.

Plan F is the most extensive since it includes virtually all out-of-pocket expenditures. It is, however, the most costly program.

Plan G provides more benefits to many beneficiaries. That's the same as Plan F, so it doesn't cover the Part B deductible, which is $183 in 2018.

Also Read: Medicare Plan G and N: What's Right for you?

When looking for Medicare Supplement options, you'll typically find that Plan G provides substantial savings over the Part B deductible. If this is the case, Plan G would be more beneficial to you.

Some plans have less coverage but are less costly each month. Plan A, for example, does not cover Parts A and B deductibles, skilled nursing facility treatment, Part B excess expenses, or international travel emergency costs. You can save money by choosing this less extensive package if you're able to pay for those costs out of pocket.

Get Medigap Quotes

Get quotes on the Medicare Supplement Plan you've selected after you've assessed your health and finances and heard about the plans and coverage levels. You won't have to compare coverage levels because they're all the same.

Our Medigap Quote will assist you in obtaining as many quotes as you need in order to make an educated decision. Pick the plans for which you want quotes after entering your zip code and other personal information.

Conclusion

You can pick the plan that's right for you now that you're familiar with the Medigap concept and your choices for Medicare Supplement plans.